How much money would investors need to target a £10,000 monthly passive income?

Different analysts will have their own opinions, but I’d suggest that £2.4m is just enough money to generate £10,000 a month. or £120,000 a year.

That’s based on having £2.4m invested in stocks, debt, bonds or active savings that collectively pay an average of 5% annually. What’s more, when this money is invested within a Stocks and Shares ISA, that income would be entirely tax free. That’s the equivalent of earnings £205,000 annually in a salaried job, given the current tax bands.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Wait! It may be easier than you think

Now, I’m sure many Britons will have zoned out when they saw the figure £2.4m. However, it’s much more achievable than many people think. The answer lies in the economics of a pension, which admittedly many people won’t be familiar with as they don’t actively manage it throughout their working career.

Nonetheless, there’s a critical component and it’s called ‘compounding’. When we invest over a long period of time, our gains compound as each year builds on the next. It may not sound like a winning strategy, but it really is.

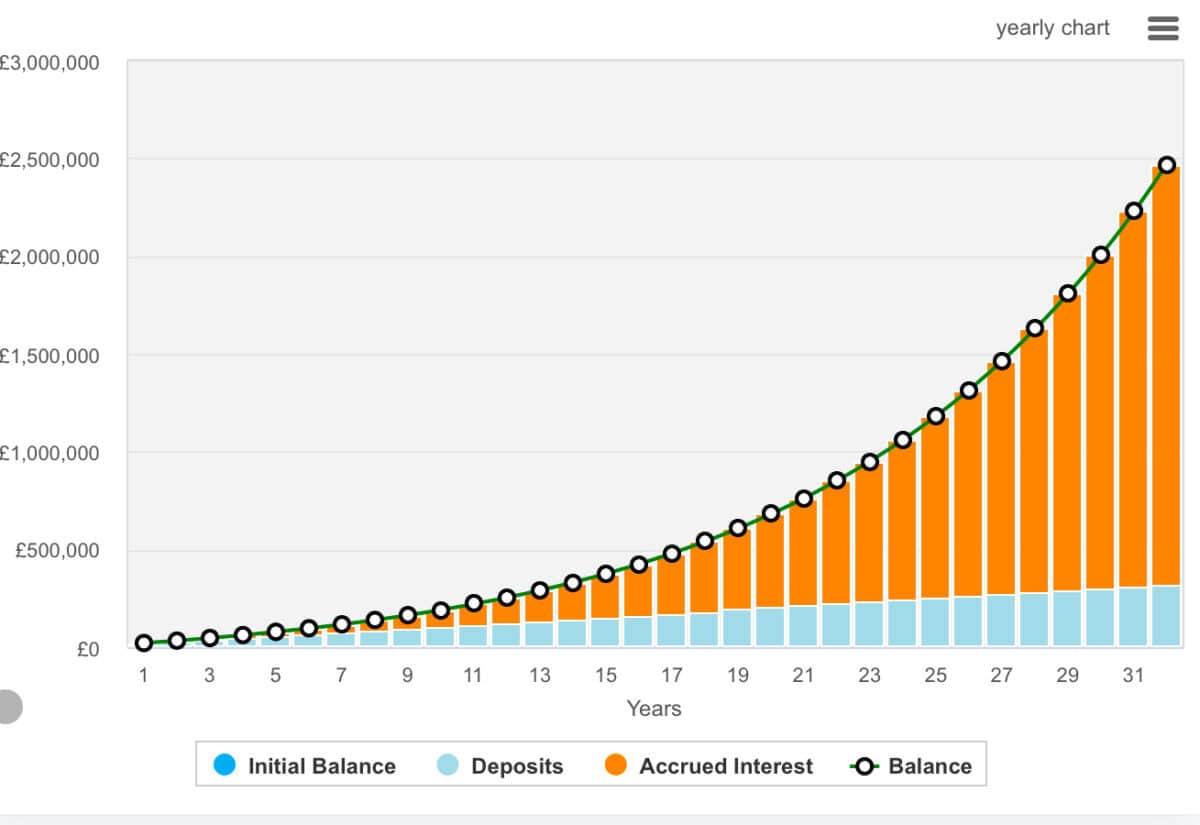

Here’s just one example of how an investor might be able to build a £2.4m portfolio:

- Initial investment of £10,000

- Monthly contributions of £800

- 32 years of consistent contributions and reinvestment

- An average annualised return of 10%

Investing well is key

The above formula is great. However, it doesn’t tell us how to invest. And if we invest poorly, we can lose money. Sadly, this is what happens to lots of novice investors looking to replicate get-rich-quick stories.

Many financial planners or analysts will start by recommending index funds — these attempt to track the performance of an index like the FTSE 100. This is a great approach to achieve diversification quickly.

However, the more adventurous may want to consider investing in individual stocks, more focused funds, or trusts. The Monks Investment Trust (LSE:MNKS) is one with interesting prospects, aiming for long-term capital growth — instead of income. This is because the fund’s managers are attracted to “businesses addressing a particular ‘crisis’ in a novel manner which can help to reduce costs and/or produce a radically improved quality of service”.

Over the past 10 years, the shares have seen 246% growth, driven by investments in companies such as Meta, Amazon, Microsoft, TSMC, and Nvidia, which also represent the five largest holdings.

However, it’s very diversified with the largest holdings all representing less than 5%. The trust’s portfolio consists of about 100 holdings across various growth profiles. As of February, it has total assets of £3,056m and a low ongoing charge of 0.44%. The trust’s dividend yield is just 0.16%.

Risks? Well, its top holdings are big tech names and some of those valuations are getting a little frothy, and some analysts will suggest that a downturn’s coming. However, over the long run, these big tech names look set to dominate.

Another risk of investing in Monks is the use of gearing (borrowing to invest). The trust can borrow money to make further investments, which can amplify both gains and losses.

In short, it’s an investment I like a lot, and it’s one I’ve added to my daughter’s Self-Invested Personal Pension (SIPP) so I feel it’s worth considering.

The post How much money would investors need to target a £10,000 monthly passive income? appeared first on The Motley Fool UK.

Should you buy The Monks Investment Trust Plc shares today?

Before you decide, please take a moment to review this first.

Because my colleague Mark Rogers – The Motley Fool UK’s Director of Investing – has released this special report.

It’s called ‘5 Stocks for Trying to Build Wealth After 50’.

And it’s yours, free.

Of course, the decade ahead looks hazardous. What with inflation recently hitting 40-year highs, a ‘cost of living crisis’ and threat of a new Cold War, knowing where to invest has never been trickier.

And yet, despite the UK stock market recently hitting a new all-time high, Mark and his team think many shares still trade at a substantial discount, offering savvy investors plenty of potential opportunities to strike.

That’s why now could be an ideal time to secure this valuable investment research.

Mark’s ‘Foolish’ analysts have scoured the markets low and high.

This special report reveals 5 of his favourite long-term ‘Buys’.

Please, don’t make any big decisions before seeing them.

More reading

- 5 FTSE 250 stocks Fools are backing for promotion to the FTSE 100 this year

- Here’s what an investor needs in an ISA to earn £5,000 of passive income a month

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Fox has positions in Nvidia and The Monks Investment Trust Plc. The Motley Fool UK has recommended Amazon, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.