3 beaten-down shares to consider buying before the next bull market

When it comes to buying shares, investors shouldn’t wait until the next bull market. The best time to look for bargains is when a lack of buyers results in lower share prices.

April has been a choppy month for stocks. But while some have recovered strongly, others are still down – and that’s where I think the opportunities are.

BP

Shares in FTSE 100 oil company BP (LSE:BP) fell 4% as the company’s earnings for the first quarter of 2025 disappointed investors. But there are also clear reasons for optimism.

Things have unraveled somewhat for the oil price in the last month. The prospect of increased supply from the US and OPEC+ is being met with weaker demand and a rising risk of recession.

That’s not good for BP. But I don’t think the long-term demand outlook for oil has changed in a meaningful way and the time to consider buying this type of stock is when things look bad.

Source: Trading Economics

The latest share buyback might be towards the lower end of expectations, but the dividend yield is almost 7%. And there’s now a lot of scope for oil prices to go higher.

JD Wetherspoon

It’s easy to see why the JD Wetherspoon (LSE:JDW) share price has been struggling recently. Increased costs are looking like a big challenge for the hospitality sector in general.

There are, however, some reasons to be positive. The latest data from the CGA RSM Hospitality Business Tracker indicates pub sales climbed 3.6% in March on a like-for-like basis.

That doesn’t sound like much, but both restaurants and bars saw sales decline. And I think JD Wetherspoon’s scale and focus on customer value makes it the best in the pub industry.

If the trend of pubs outperforming other parts of the hospitality sector continues, the company could surprise people. As a result, I think it’s worth considering at today’s prices.

Disney

I’ll be interested to see what happens when Disney (NYSE:DIS) reports earnings next week. US economic data has been weak recently and this could be a risk for the company.

A decline in tourism might mean fewer visitors to its theme parks. And in its previous update, the firm reported a decline in the subscriber base for its streaming services.

Over the long term, however, I think things look much more positive. Disney has some outstanding intellectual property and this should be extremely valuable over time.

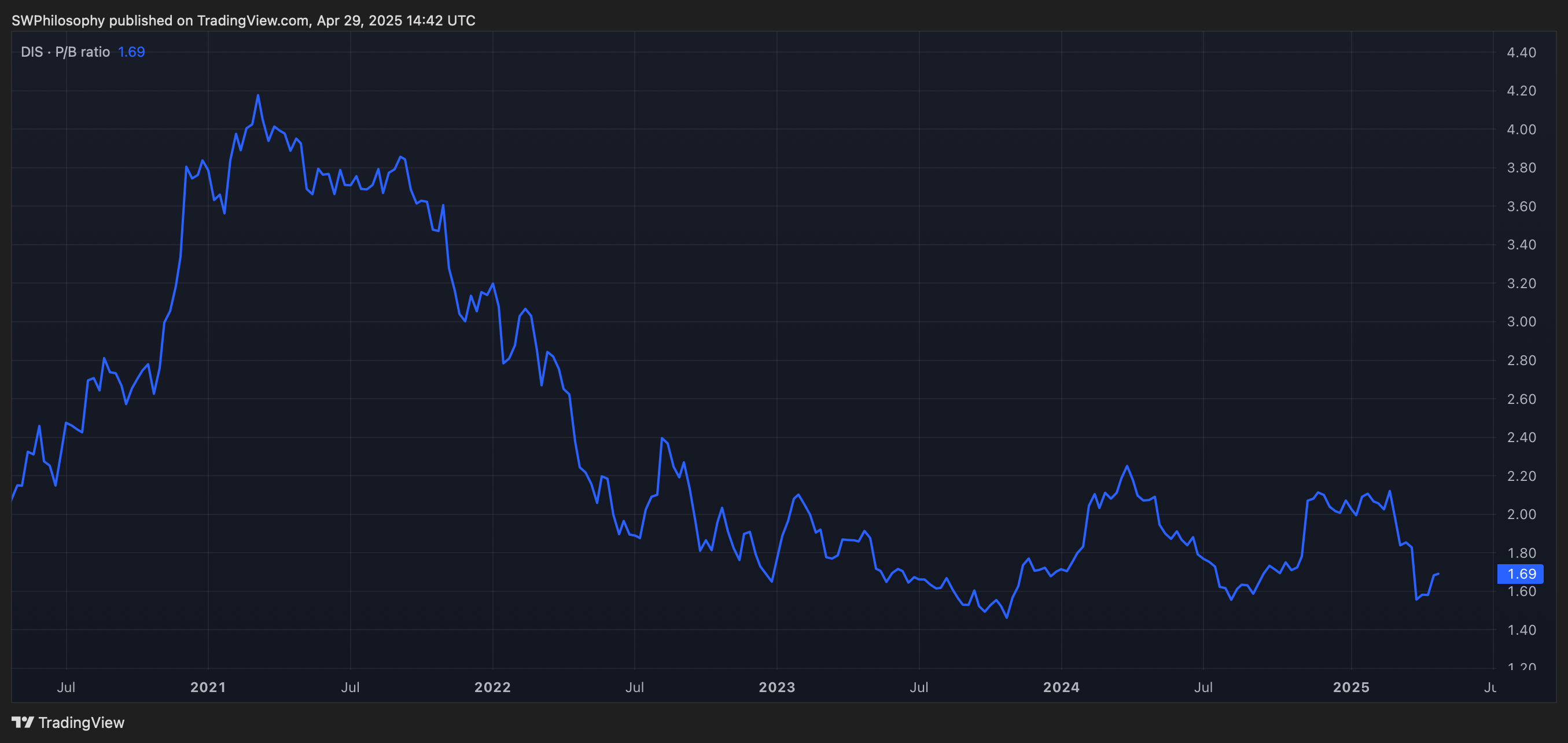

Created at TradingView

On the subject of those assets, the stock is trading at an unusually low price-to-book (P/B) ratio. Things might get worse in the short term, but this could be a good time for long-term investors to consider buying.

When?

The oil price recovering from its recent fall could push BP’s profits higher. If that happens, I expect investors to do well.

Sales at JD Wetherspoon might also grow more than some people are expecting. And that could help offset the increasing costs the company is facing.

Disney’s intellectual property is second to none. So while a recession might not be good for the company, I think the long-term picture is much brighter.

I don’t know when share prices are going to pick up, but waiting for the next bull market to start is risky. Instead, I think investors should look for stocks to consider buying now.

The post 3 beaten-down shares to consider buying before the next bull market appeared first on The Motley Fool UK.

5 Shares for the Future of Energy

Investors who don’t own energy shares need to see this now.

Because Mark Rogers — The Motley Fool UK’s Director of Investing — sees 2 key reasons why energy is set to soar.

While sanctions slam Russian supplies, nations are also racing to achieve net zero emissions,

he says. Mark believes 5 companies in particular are poised for spectacular profits.

Open this new report — 5 Shares for the Future of Energy

— and discover:

- Britain’s Energy Fort Knox, now controlling 30% of UK energy storage

- How to potentially get paid by the weather

- Electric Vehicles’ secret

backdoor

opportunity - One dead simple stock for the new nuclear boom

Click the button below to find out how you can get your hands on the full report now, and as a thank you for your interest, we’ll send you one of the five picks — absolutely free!

More reading

- Will these Q1 results mark the turning point for the BP share price?

- BP shares now yield nearly 7% a year and look 72% undervalued to me as well!

- Outlook: in just 12 months the BP share price could turn £10,000 into…

- BP shares go ex-dividend on 15 May. Time to consider grabbing that 6.5% yield?

- 2 FTSE 100 shares I’m avoiding like the plague right now

Stephen Wright has positions in J D Wetherspoon Plc and Walt Disney. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.