Here’s how to target a £20m SIPP, but it’s not for you…

While a £20m SIPP (Self-Invested Personal Pension) may sound like fantasy, it can be a reality. However, the concept becomes more plausible when reframed over a very long timescale. The key is compounding, and the best time to start is at birth.

Although a baby can’t open a SIPP themselves, a parent or guardian can do so on their behalf. Under current UK rules, up to £2,880 a year can be contributed to a child’s SIPP, and with tax relief this becomes £3,600.

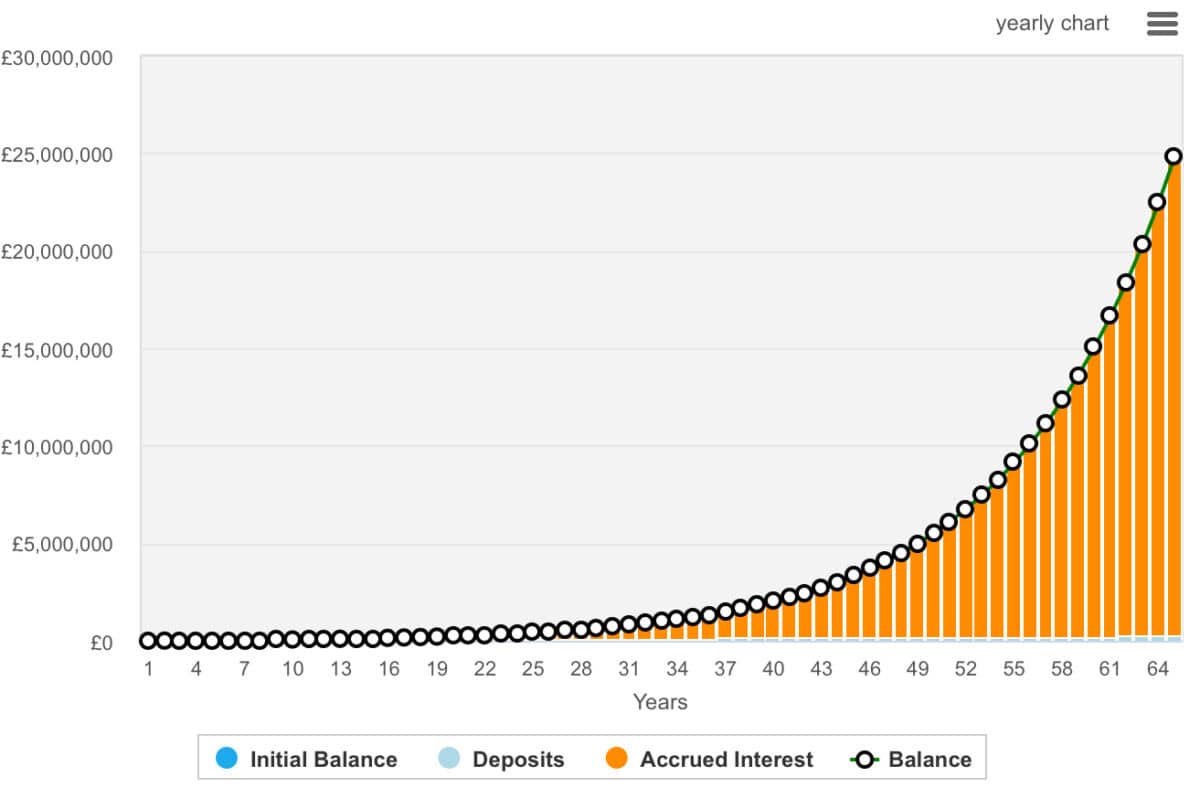

It may not sound like much, but this £240 (plus £80 from the state) a month can compound over time if invested wisely. Placed into a low-cost global equity tracker — assuming an average 8% annual return — and by age 65, the pot could exceed £8m.

However, if the rate of return is a little stronger, say 10%, that figure after 65 years jumps massively to £24m! But this is by no means guaranteed. The value of money invested in stocks can fall or the return might be much lower, so those millions might be out of reach!

But I assume constant contributions and a child increasing those contributions when they’re working. After all, £240 is unlikely to be a large commitment in 20/30 years (they would still receive tax relief).

Of course, that’s a long-term projection and the child wouldn’t be able to access the funds until their 50s, at least. But the point remains: starting early unlocks huge potential via the power of compounding.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

This is generational wealth

This strategy won’t appeal to everyone. It requires patience, discipline, and a long time horizon that those currently reading this won’t have — which is why, as my headline says, “it’s not for you.” But for those thinking generationally, a baby’s SIPP could be the cornerstone of an extraordinary retirement future.

Combined with a Junior ISA, this could provide a child born today with an extraordinary future. And hopefully one that involves very little financial stress.

Where to invest?

When it comes to building long-term wealth inside a SIPP, especially one opened for a child, the choice of investments matters enormously.

My daughter’s SIPP, for example, contains several trusts and conglomerates, but also a couple of handpicked, high-conviction stocks. One of which is Celestica (NYSE:CLS).

I added this stock to my daughter’s portfolio around 18 months ago as her first single company investment. Why? It was simply vastly undervalued, trading around 14 times forward earnings but with an earnings growth rate of near 30%.

The result has been around 700% growth since the initial investment. Now, not every stock pick has to be a big winner, but I believe this one’s reflective of what can happen if investors focus on metrics. What the numbers say should underpin every investment we make.

Risks? Well, the current valuation is one. But it’s also worth noting that with production facilities in East Asia, the company’s highly exposed to changes in US trade policy.

However, the stock remains part of my daughter’s portfolio. But I’m not adding any more right now. The valuation has become very hot. However, as an integral part of the artificial intelligence (AI) value chain, it’s something I may top up on if we see a correction. I think other investors could do the same.

The post Here’s how to target a £20m SIPP, but it’s not for you… appeared first on The Motley Fool UK.

More reading

- 2 potential buy-and-hold US stocks for the AI revolution

- Up 134% in 2025, is this FTSE stock the new Rolls-Royce?

- Fresnillo shares jump as profit surges. Is this still one of the best FTSE 100 stocks to buy?

- Here are the latest share price forecasts for Lloyds, Barclays and HSBC

- The Smith & Nephew share price is up 14% today. Here’s why the FTSE 100 stock could be just getting started

James Fox has positions Celestica Inc. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.