This FTSE 100 defence contractor’s share price is wobbling… but I’m not selling up

The share price of FTSE 100 military contractor Babcock International Group (LSE:BAB) has had a terrible few weeks. On nine of the 12 trading days to 16 October, itâs fallen. And at the time of writing (mid-morning 17 October), the stock’s having another bad day. The groupâs now worth nearly 15% less than it was at the start of the month.

Whatâs caused this drop? Well, I think itâs more than a coincidence that — on 30 September — President Trump announced that Israel and Hamas âhave signed off on the first phaseâ of a 20-point peace plan for Gaza.

Conflicted by conflict

And to be honest, this is troubling my conscience. I justify being a shareholder because I believe a government should protect its people. Iâm not looking to profit from war.

Instead, my goal is to take advantage of the UKâs plans to increase defence expenditure. Earlier this year, it said it was to spend 2.5% of GDP on the countryâs army, navy and air force by 2027. It also âcommittedâ to reaching the NATO target of 3.5% by 2035.

During the year ended 31 March (FY25), Babcock earned 71% of its revenue from the UK. To help boost economic growth, the government prefers to âspend localâ when it comes to military expenditure. On this basis, the group looks set to benefit.

Yet this monthâs share price movement provides strong evidence that investors are selling up because thereâs a belief that the current conflict in the Middle East is coming to an end. The value of my shareholding is falling because others donât think peace is good for the group.

A bit of a puzzle

However, from a financial perspective, this doesnât make sense. As far as I can tell, Babcock doesnât sell anything to Israel. Some other British companies supply parts for the F-35 bomber made by Lockheed Martin thatâs used by the Israeli air force. But most export licences were suspended in September 2024.

And regardless of whether thereâs peace in the Middle East or, indeed, Ukraine, as I certainly hope, NATO members have agreed to spend more protecting themselves. It’s a sad reality that we live in a dangerous world. This means the defence sectorâs likely to experience significant growth over the next decade.

All guns blazing

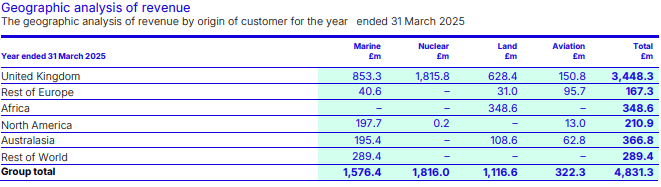

Babcock’s enjoyed tremendous growth over the past few years. It upgraded its medium-term guidance in June. Itâs now targeting a one percentage point improvement in its operating margin which, based on its reported revenue in FY25 of £4.8bn, could be worth nearly £50m of additional earnings.

However, the group disappointed when delivering a recent contract for the Royal Navy. It incurred unexpected costs of £190m. This was so significant that it was reported as a separate item within its accounts. Itâs also a reminder of how difficult its operations can be.

And the groupâs dividend is a little mean. The stockâs presently yielding 0.6%.

But Iâm planning on retaining my shares. And I think others could consider adding the stock to their own portfolios because itâs operating in a growing market, trades at a lower earnings multiple than most of its contemporaries, and has an order book worth £10.4bn (at 31 March). And thatâs regularly being topped up with new contract wins.

The post This FTSE 100 defence contractor’s share price is wobbling⦠but I’m not selling up appeared first on The Motley Fool UK.

Should you invest £1,000 in Babcock International Group PLC right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Babcock International Group PLC made the list?

More reading

- Up 137% and 72%, these FTSE 100 growth stocks have smashed Lloyds shares!

- Rolls-Royce, Babcock and BAE Systems share prices are all falling today! Time to consider buying?

- The Rolls-Royce share price is flying but investors might consider buying this FTSE 100 growth star first

- Time to buy the FTSE 100âs 2 best performers of 2025?

- European defence stocks are booming so what has the FTSE 100 got to offer?

James Beard has positions in Babcock International Group Plc. The Motley Fool UK has recommended Lockheed Martin. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.