Why high valuations aren’t a reason for investors to stop buying stocks

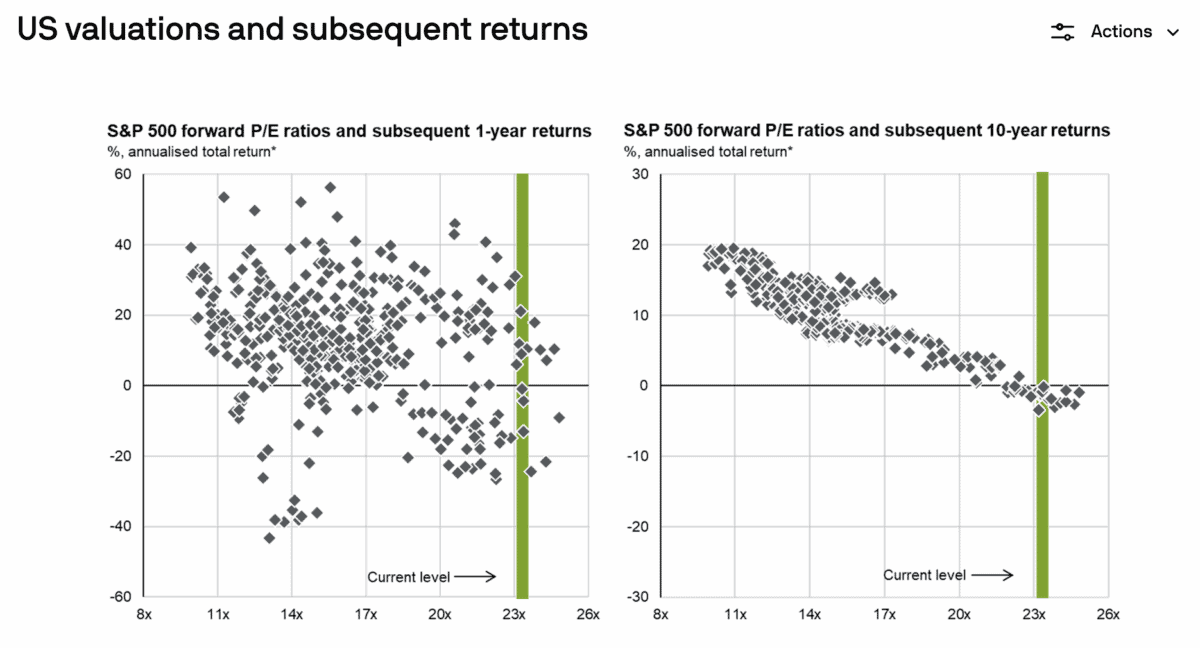

The S&P 500 is trading at a valuation that usually leads to weak returns for 10 years, but I donât think investors should stop buying stocks. In fact, I think this would be a big mistake.

Source: JP Morgan Q4 Guide to the Markets

I donât have any argument with the data and Iâm half expecting a difficult year for the stock market in 2026. So why do I think investors should keep investing?

Cost averaging

A lot of investors follow a strategy known as cost averaging. This involves buying shares with a fixed amount on a regular basis, regardless of whatâs going on with prices.

One of the best things with this approach is it removes any concerns about valuations. It doesnât matter whether stocks are cheap or expensive, you just buy regularly and consistently.

It works as long as share prices go up over time. Investors end up with a cost basis in line with the historical average and they make money as long as stocks eventually go higher.

For anyone using this method, high share prices are no reason to stop buying. The plan is valuation-agnostic, so investors shouldn’t see this as important.

Value investing

Some investors, however, have strategies that do focus on valuations. And for anyone taking this type of approach, high price-to-earnings (P/E) ratios are something to pay attention to.

Iâm in this position â Iâm very uneasy at the idea of buying stocks at prices that I think are too high. But the solution for investors like me is straightforward â just donât buy the S&P 500.

There are literally hundreds of individual stocks to consider at the moment. And the fact the US index as a whole is historically expensive doesnât mean all of its constituents are.

In fact, the S&P 500 has become extremely concentrated around a few artificial intelligence (AI) names. But beyond these, there are a number of stocks that donât look expensive at all.

Energy

One of the worst-performing sectors from the S&P 500 has been energy. But I think investors interested in valuations might look at the likes of ConocoPhillips (NYSE:COP) as a result.

Falling oil prices have been â and remain â a potential risk. But I think the company is in a strong position to withstand a downturn in commodity prices.

The firmâs assets typically have production costs between $30 and $35 a barrel. Its balance sheet is also strong, which should help with its resilience. And then thereâs the dividend.Â

Despite falling prices, ConocoPhillips has returned almost $7bn to investors since the start of 2025. At its current market value, thatâs a 6.5% return so far this year with more to come in Q4.

Opportunities

In general, high valuations arenât a reason to stop buying stocks. For anyone looking to cost average, this is part of the plan and I think there are also opportunities for value investors.

Itâs surprising to me that the US energy sector has struggled when one of the main challenges to AI growth in 2026 is how to power data centres. But I see attractive valuations there.

ConocoPhillips is one name that I think investors could consider. But for my own portfolio, thereâs a slightly riskier oil stock outside the S&P 500 that I like even more at todayâs prices.

The post Why high valuations aren’t a reason for investors to stop buying stocks appeared first on The Motley Fool UK.

Should you invest £1,000 in ConocoPhillips right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if ConocoPhillips made the list?

More reading

- These 3 jaw-dropping FTSE 100 dividend stocks have 1 brilliant thing in common

- How much do you need in an ISA to take £23,184 per year as a passive income?

- These 3 high-yield income stocks boast a stunning 10-year dividend track record!

- How on earth are Rolls-Royce shares up 1,556% since 2022?

- Could these dirt-cheap FTSE 250 shares enjoy a December rebound?

JPMorgan Chase is an advertising partner of Motley Fool Money. Stephen Wright has no position in any of the shares mentioned. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.