Could this FTSE 100 stock be a major winner from the Autumn 2025 Budget?

Ahead of todayâs (26 November) Autumn Budget, I was reminded of a Ronald Reagan quote. In 1986, the former US President said the nine scariest words in the English language were: âIâm from the government, and Iâm here to help.â

And in my opinion, all the leaks and speculation in the run up to the Chancellor’s speech were far from helpful. Indeed, Andy Haldane, the former chief economist at the Bank of England recently said that the governmentâs approach to the Budget has been âsucking all lifeâ out of the economy. Not good.

But now that Rachel Reeves has sat down in the House of Commons, we finally have some clarity. And although there will inevitably be some losers from any Budget, I think the UKâs housebuilders could be among the net beneficiaries.

Thatâs because early indications are that the gilt market approves of the Chancellorâs package of measures. When the Office for Budget Responsibility’s report was accidentally published too early, the yield on 10-year government debt increased. But since then, it’s started to fall, which suggests bond investors are more relaxed about the Budget than initially feared.

One to consider

Changes in gilt rates generally feed through to the cost of mortgages. And this should help Persimmon (LSE:PSN). If borrowing costs fall it’s likely to help the housing market, which is starting to show signs of picking up after its post-pandemic slowdown.

The most recent report from the Bank of England revealed that net borrowing of mortgage debt by individuals rose by £1.2bn to £5.5bn in September. This was the highest since March 2025. The central bank also noted that the interest rate on newly drawn mortgages was the lowest since January 2023. This is likely to fall further if the current gilt market trend continues.

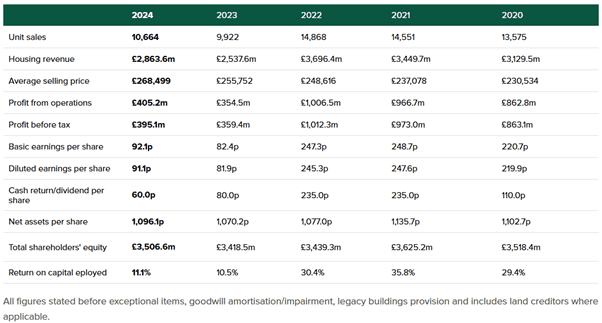

In its November trading statement, Persimmon said it was on target to meet the 2025 market consensus of 11,293 completions and an underlying profit before tax of £429m.

Early during the Chancellor’s speech, investors marked down the share prices of the UKâs housebuilders. I suspect they were disappointed that she didn’t announce any changes to stamp duty or introduce measures to help first-time buyers.

Alternatively, they may think the housing market recovery could stall. Also, they might be concerned that inflation is continuing to erode margins in the sector. I acknowledge these are both risks.

However, I remain optimistic about Persimmonâs prospects. Its properties have a lower average selling price than its peers. Also, its balance sheet is debt-free. In addition, it’s got plenty of plots on which to build. And with a yield of 4.6%, it’s good for income too.

Thatâs why, on balance, I think Persimmon could be worth considering.

On reflection

Finally, I think itâs worth noting that, from April 2027, the annual Cash ISA limit will be cut from £20,000 to £12,000 (for under-65s only). The government wants to encourage people to put more of any spare cash they have into a Stocks and Shares version.

Personally, I think thatâs a good idea. Inflation is permanently eroding the value of cash and history tells us that by investing in quality stocks over the long term, the returns are likely to be greater. And in my opinion, there are plenty of these to choose from.

The post Could this FTSE 100 stock be a major winner from the Autumn 2025 Budget? appeared first on The Motley Fool UK.

Should you invest £1,000 in Persimmon Plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Persimmon Plc made the list?

More reading

- How might the UK Autumn Budget affect our favourite FTSE 100 shares?

- Plenty of stocks are forecast to grow faster than the Rolls-Royce share price. Here are just 3

- 2 UK shares I’d prefer to own over Lloyds stock right now

- Prediction: in 12 months the Persimmon share price and dividend could turn £10,000 into…

- After a strong Q3 update, is the Persimmon share price too cheap to ignore?

James Beard has positions in Persimmon Plc. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.</a>