The BP share price is back above 500p — but is there more to come?

The BP (LSE: BP.) share price has spent years in the doldrums. A costly detour into renewables, heavy buybacks that stretched the balance sheet, and a prolonged slump in oil prices left investors frustrated and the stock drifting.

For much of the past year, crude hovered around $55 a barrel, and sentiment towards oil majors remained distinctly bearish.

But in just a couple of months, the picture has changed dramatically.

Oil prices had been creeping higher since the start of the year, and today (2 March) Brent crude surged 8% to around $80 amid escalating tensions in the Middle East.

Energy markets are now rapidly repricing supply risk, and early trading pushed the stock above 500p, its highest level in three years.

The question for investors is clear: is this merely another short-term bounce or the start of a far bigger comeback?

A business that still generates serious cash

Despite headlines around suspended share buybacks and a $4â¯bn impairment â mostly tied to low-carbon assets â its cash metrics remained strong.

Operating cash flow was $24.5â¯bn, underlying replacement cost profit $7.5â¯bn, and net debt fell to $22.2â¯bn. Even in a weak oil environment, BP can generate real cash.

Managementâs medium-term targets assumed Brent at roughly $74 a barrel. With crude now pushing $80, the financial maths shifts. Higher prices feed directly into upstream margins and free cash flow, easing concerns over dividend cover and debt reduction.

In short, even when oil was weak, it was resilient. At $80, upside for cash flow, dividends, and potentially the share price looks more credible.

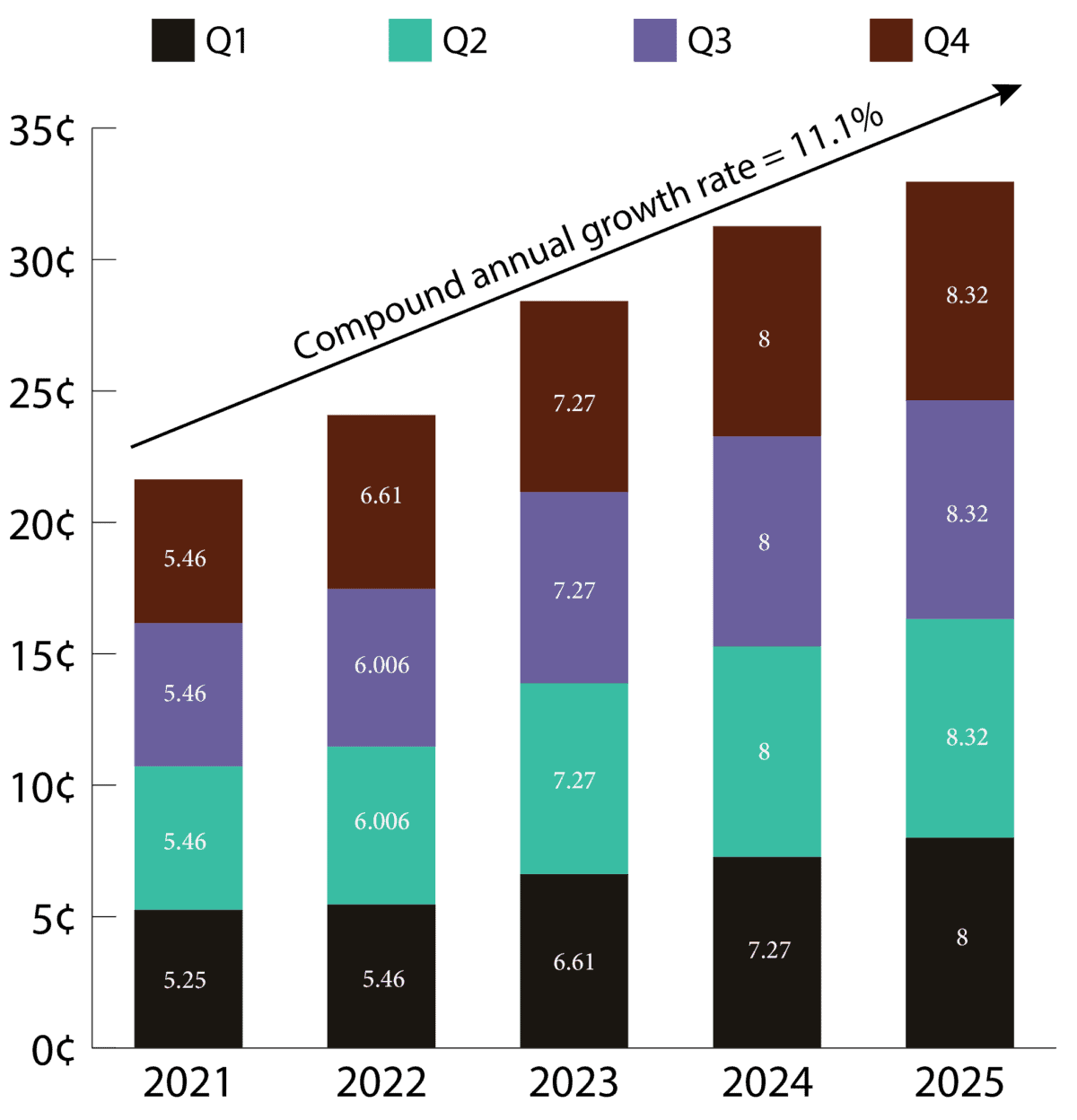

Dividends

The dividend remains central to the investment case. Although still below pre-2020 levels, the chart below shows that over the past five years the payout has risen from 21.63â¯Â¢ to 32.96â¯Â¢, a compound annual growth rate of over 11%.

Chart generated by author

Since 2021, the dividend has consumed less than half of free cash flow, so it has been supported by real cash generation.

This underpins the stockâs appeal for income-focused investors, particularly those holding the shares in a Stocks and Shares ISA where dividends compound tax-free.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Risks

BP faces a range of non-price risks though. These include regulatory pressures, potential tax or royalty changes, project delays, operational incidents, and challenges in executing its capital-allocation strategy. Even with strong cash flow, these factors could affect earnings, dividend sustainability, and investor sentiment, highlighting that the stock isn’t without exposure to unforeseen events.

Strategy and demand backdrop

The ‘peak oil’ narrative is fading. Markets assumed global demand would peak by 2030, shaping valuations and driving aggressive renewable pivots. But demand remains resilient: AI-driven data centres, emerging-market growth, and slow nuclear deployment mean hydrocarbons will stay central.

BPâs strategy reset reflects this. Itâs focused on upstream growth, adding 150,000 barrels per day from six projects in 2025, while the Bumerangue discovery in Brazil strengthens its long-term production pipeline.

In todayâs environment of elevated inflation and rising geopolitical tensions, oil and gas have proven their value. BPâs performance shows why the sector can help support a portfolio even when broader markets are under pressure.

For me, this resilience â combined with strong cash generation and a growing dividend â is a core reason BP remains a key holding in my ISA portfolio. For others, I see it as a stock to watch closely.

The post The BP share price is back above 500p â but is there more to come? appeared first on The Motley Fool UK.

Should you invest £1,000 in BP p.l.c. right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if BP p.l.c. made the list?

More reading

- The BP and Shell share price are soaring today â are we looking at another massive spike?

- Iâve bought these 3 brilliant dividend stocks to target a high and rising monthly ISA income

- I asked ChatGPT for its top 5 FTSE 100 stocks to buy for March 2026

- Just a £5,000 holding in BP shares could generate £1,807 in annual income for investors over time!

- £1,000 invested in BP shares 1 year ago is now worth…

Andrew Mackie has positions in Bp P.l.c. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.