With a P/E of 9.5 and 7.4% dividend yield, is this FTSE 250 stock a no-brainer?

The FTSE 250 is stuffed full of dividend shares, including over 20 offering a return of 7% or more. But what if one of them also had a current (2 March) earnings multiple of just 10?

Would this make it a bit of a no-brainer buy? Or could it all be too good to be true? Letâs find out.

The big reveal…

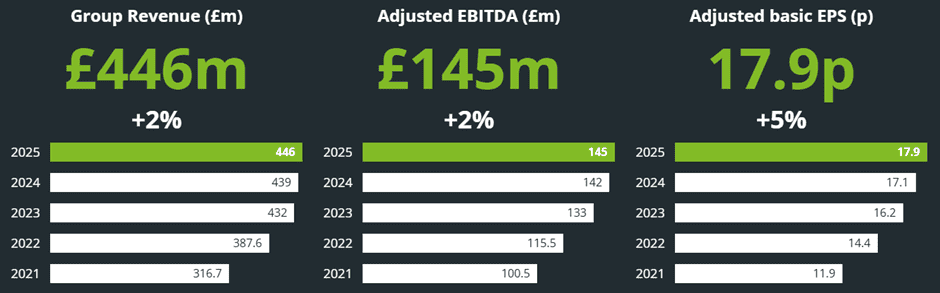

MONY Group (LSE:MONY) owns six brands, which it claims saved consumers £2.8bn in 2025. It earns revenue by transferring users of its websites and apps to third-party providers of insurance, money, home services, and travel products.

Its most famous brands are probably MoneySuperMarket and MoneySavingExpert, which the group bought from Martin Lewis (once described as the most trusted man in Britain) in 2012.

Since the pandemic, the groupâs been steadily growing its revenue and earnings. Comparing 2025 with 2021, turnover was up 40.8% and adjusted basic earnings per share (EPS) was 50.4% higher. Over the same period, it raised its dividend by 7.9% in cash terms.

Although the stockâs consistently offered a return higher than the FTSE 250 average, a falling share price â itâs down 40% since March 2021 — has lifted its yield higher. Based on its 2025 total payout, the stockâs presently yielding 7.4%, compared to 3.4% for the index as a whole.

| Financial year | Share price (pence) | Adjusted basic EPS (pence) | Price-to-earnings ratio | Dividend (pence) | Yield (%) |

|---|---|---|---|---|---|

| 31.12.21 | 216 | 11.9 | 18.2 | 11.71 | 5.4 |

| 31.12.22 | 192 | 14.4 | 13.3 | 11.71 | 6.1 |

| 31.12.23 | 280 | 16.2 | 17.3 | 12.10 | 4.3 |

| 31.12.24 | 192 | 17.1 | 11.2 | 12.50 | 6.5 |

| 31.12.25 | 184 | 17.9 | 10.3 | 12.63 | 6.9 |

As well as appearing to be great for passive income, the stock also looks attractive from a valuation perspective. Itâs now trading at 9.6 times its 2025 EPS. This is well below its five-year high of over 18.

And if the analystsâ forecasts prove to be accurate, the groupâs price-to-earnings ratio looks set to fall further over the next two years, to 9.1 (2026) and 8.6 (2027).

With several strong brands, a solid business proposition (who doesnât want to save money?), a generous dividend (no guarantees), and cheap valuation, whatâs not to like about the MONY Group?

A rapidly changing landscape

Well, it appears to be suffering from a shift in sentiment towards asset-heavy stocks — remove intangibles from its 31 December 2025 balance sheet and it would have a negative book value.

And it was recently caught by the fallout from the news that US tech business Insurify has developed an artificial intelligence (AI) tool that allows users to compare car insurance prices using ChatGPT.

At one point in February, MONY Groupâs share price fell to its lowest level in 13 years.

Since then, the groupâs sought to reassure investors by launching its own ChatGPT-based app.

And itâs reconfirmed that it sees AI as a way of cutting costs and increasing revenue rather than as a threat. MONY Groupâs boss recently said: “Our leading data and tech architecture… has positioned us exceptionally well to harness the opportunity of AI“.

This is important and I think it will go a long way to reassure investors. Personally, this news has also resulted in me changing my view about the groupâs prospects. The new app addresses my previous concerns that its business model will be disrupted by AI.

Now, with its healthy dividend and historically attractive valuation — on balance — I believe MONY Group’s one to consider. Of course, no stock’s a complete no-brainer but, in this case, after weighing up the pros and cons, I think now could be a good buying opportunity.

The post With a P/E of 9.5 and 7.4% dividend yield, is this FTSE 250 stock a no-brainer? appeared first on The Motley Fool UK.

Should you invest £1,000 in Mony Group Plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Mony Group Plc made the list?

More reading

- The Dow Jones may be at 50k but these 3 UK shares are forecast to grow further in 2026

- Does AI disruption mean these 3 cheap shares are bargain buys right now?

- Hereâs how investors can target £22,491 a year from £20,000 in this overlooked income share

James Beard has no position in any of the shares mentioned. The Motley Fool UK has recommended Mony Group Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.