1 of the top UK growth stocks to consider buying in April

Growth stocks trading at discounted valuations can be huge opportunities for investors. And thereâs one in particular thatâs catching my eye. The stock’s gone nowhere for the last five years, but the underlying business has done well. So I think itâs time to take a closer look.Â

Filtration

The company in question is Porvair (LSE:PRV). The firm manufactures filtration equipment for the aerospace and laboratory equipment industries.

There are several reasons I like this business, including:

- Strong repeat business.

- High barriers to entry.

- Resilient revenue streams.

- Impressive cash conversion.

Letâs take a closer look at each of these.

In the aerospace industry, Porvairâs filters have to be replaced after a certain time. This isnât optional â itâs a legal requirement. With lab equipment, a lot of the companyâs products are designed to be used once. That leads to a steady stream of repeat sales.

Its industries are have high regulatory standards. Whether itâs aircraft, drug development or water purity, competing isnât straightforward. That makes it difficult (or impossible) for customers to switch to alternative providers. And that generates good pricing power for Porvair.

In terms of cyclicality, it’s important that the firm’s products are typically maintenance expenses. That makes demand fairly stable, even when companies aren’t expanding.

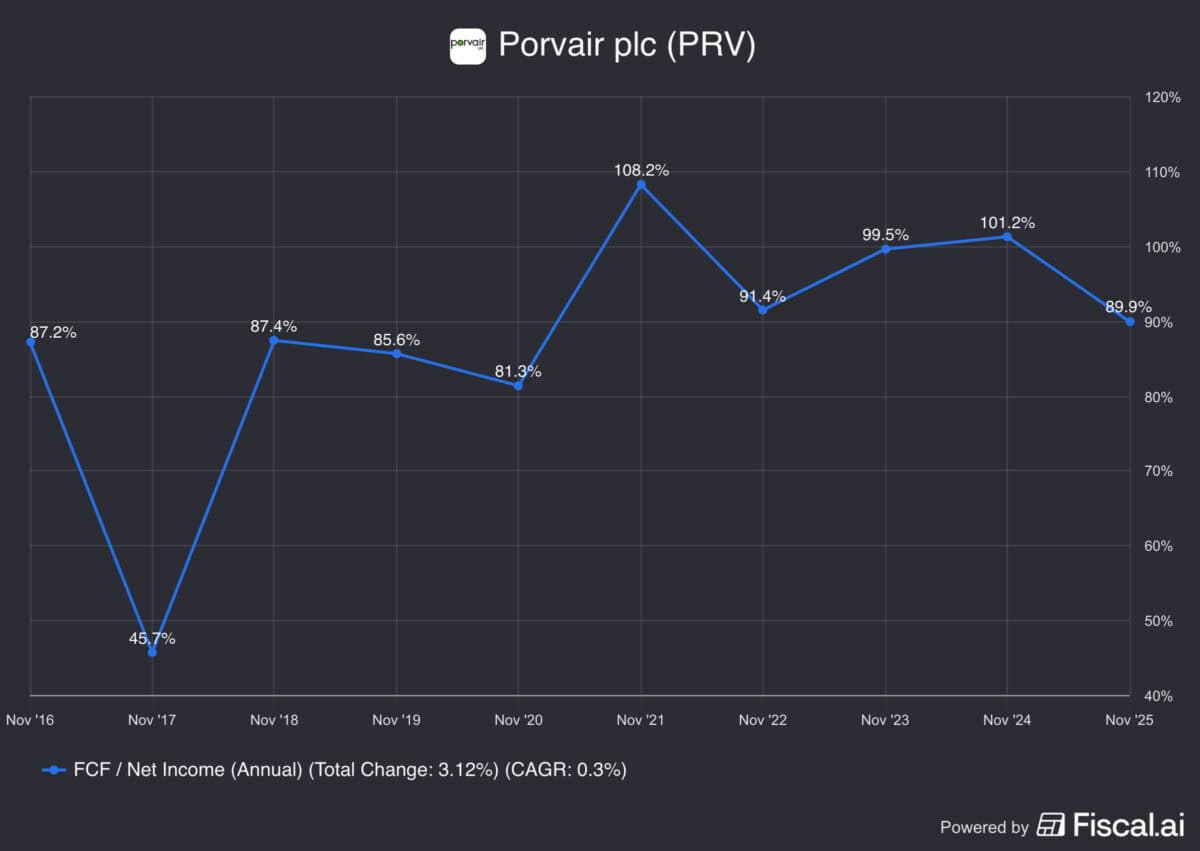

Source: Fiscal.ai

The firm also has excellent cash conversion metrics. Over the last 10 years, itâs consistently turned over 75% of its net income into free cash.

Dead money?

This all sounds positive, but it raises an obvious question. If the business is so good, why has it essentially gone nowhere since 2021?

The reason’s twofold. One’s growth â Covid-19 created a surge in demand for lab equipment that hasnât been maintained since. As a result, Porvair’s had to contend with higher inventory levels and weaker demand. And this has been a challenge for the business.

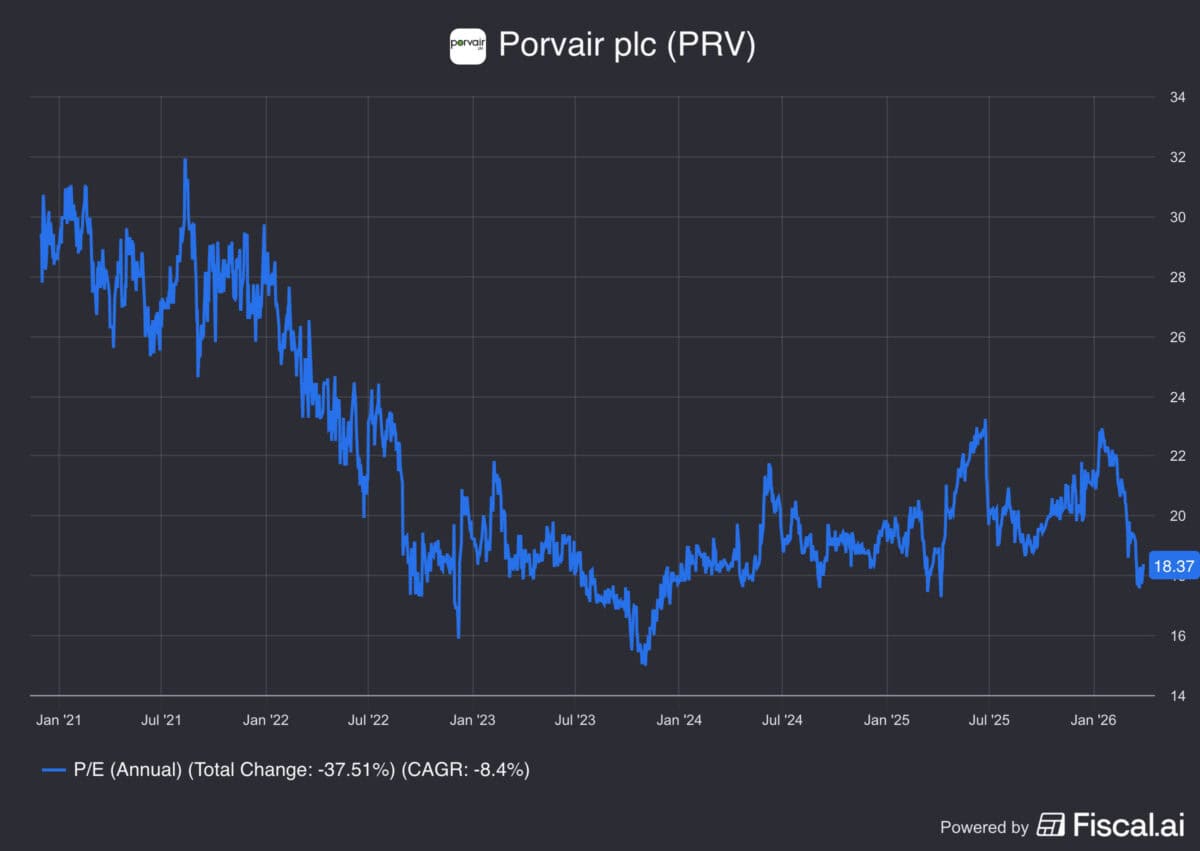

The second’s valuation. Five years ago, the stock was trading at a price-to-earnings (P/E) ratio of 27, which is pretty high. As Warren Buffett points out, itâs possible to pay too much even for an outstanding business. And I think this might have been the case in 2021.

Now however, things are different on both fronts. Demand for lab filters started to recover in 2025 after a long period of high inventory levels.

Source: Fiscal.ai

On top of this, the stock’s now trading at a P/E multiple below 18. So I think the business has had enough time to catch up with the share price.

Risks and opportunities

Porvair shares are down 15% since the start of the year. And a big reason for this is the ongoing conflict in the Middle East. The firm’s relatively well-protected from cyclical ups and downs, but it isn’t immune to a global recession and thatâs a risk right now.

From a long-term perspective though, thereâs a lot to like about the business. And the current share price looks attractive to me. Opportunities like this donât come around often, so I think investors should give this one serious consideration right now.

The post 1 of the top UK growth stocks to consider buying in April appeared first on The Motley Fool UK.

Should you invest £1,000 in Porvair plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Porvair plc made the list?

More reading

- Is this the best time to buy shares in a long time?

- £1,000 buys 35 shares in an incredibly reliable FTSE 100 dividend stock

- This is what Warren Buffett has to say about passive income — and I’m listening!

- 2 excellent ETFs to consider buying for an ISA in April

- How much would someone need in an ISA to target £308,538 annual dividend income?

Stephen Wright has no position in any of the shares mentioned. The Motley Fool UK has recommended Porvair Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.