A dirt-cheap FTSE 250 growth AND dividend share to consider in February!

Looking for low-cost FTSE 250 growth and income shares to buy? Residential landlord Grainger (LSE:GRI) might be just the ticket.

Here’s why I think it merits serious consideration today.

Strong conditions

A chronic property shortage has driven residential rents skywards in recent years. As Britain’s largest listed rental accommodation provider, Grainger has been a huge beneficiary of this upswing.

It’s rapidly grown its property portfolio to capitalise on this, and now has more than 11,000 homes on its books. That compares with around 5,600 homes five years ago.

The big question for investors today is whether this trend can continue. Falling demand more recently has caused some room for doubt: according to Rightmove, average advertised UK rents outside London dropped 0.2% in the last quarter of 2024.

With elevated rental costs squeezing the number of prospective tenants, advertised rents (excluding the capital) dropped for the first time since 2019.

This could be the beginning of a trend that threatens profits at Grainger and its peers. The government’s plans to build 1.5m new homes during the five years to 2029 might also dent profits growth.

But I’m not so sure. First and foremost, this is because Britain’s population is booming and tipped to continue doing so, driving demand for residential space significantly higher.

The Office for National Statistics (ONS), for instance, predicts the UK population will grow by around 5m between 2022 and 2032, to 72.5m.

At the same time, the number of buy-to-let investors is falling due to rising costs and regulatory hoops. Estate agent Hamptons has predicted 113,630 new buy-to-let purchases across the UK in 2024, down a whopping 40% in less than a decade.

Growth to accelerate?

Grainger isn’t without risk, especially given the threat of interest rate pressures persisting that crimp asset values.

But on balance, I think the earnings picture here is largely very bright. This is backed up by current broker forecasts: City analysts think earnings will rise 2% during the financial year to September 2025 before growth accelerates to 10% in fiscal 2026.

Now, Grainger shares don’t look cheap based on these figures. For this financial year, they trade on a price-to-earnings (P/E) ratio of 22.1 times.

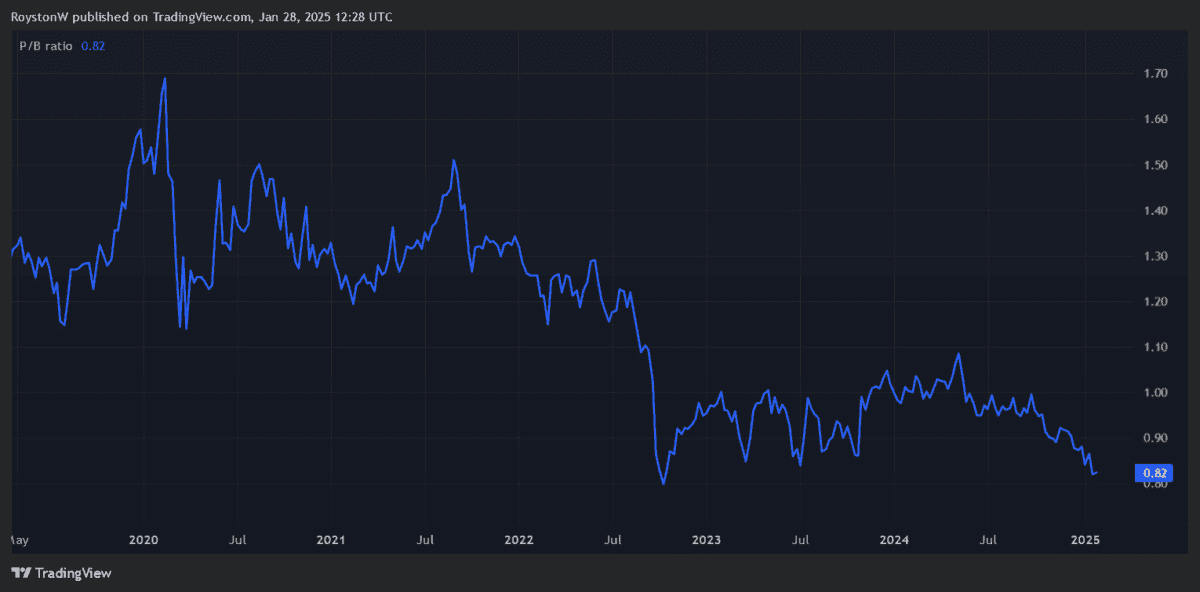

However, based on another popular value metric — the price-to-book (P/B) ratio — the FTSE 250 share actually looks exceptionally cheap.

With a reading below 1, at 0.8, the landlord trades at a discount to the value of its assets.

Rising dividends

Pleasingly for Grainger investors, the prospect of solid profits growth means City analysts expect dividends to continue rising sharply over the forecasted period.

For financial 2025 and 2026, total dividends are tipped to soar 12% and 9%, respectively. To put that in context, shareholder payouts across the broader stock market are expected to grow between 4% and 4.5%.

What’s more, these predictions push Grainger’s dividend yields to 4% for 2025 and 4.4% for 2026. Both figures comfortably beat the 3.3% average for FTSE 250 shares.

For investors seeking a blend of growth, income, and value, I think Grainger shares are worth a close look.

The post A dirt-cheap FTSE 250 growth AND dividend share to consider in February! appeared first on The Motley Fool UK.

Investing in AI: 3 Stocks with Huge Potential!

🤖 Are you fascinated by the potential of AI? 🤖

Imagine investing in cutting-edge technology just once, then watching as it evolves and grows, transforming industries and potentially even yielding substantial returns.

If the idea of being part of the AI revolution excites you, along with the prospect of significant potential gains on your initial investment…

Then you won’t want to miss this special report inside Motley Fool Share Advisor – ‘AI Front Runners: 3 Surprising Stocks Riding The AI Wave’!

And today, we’re giving you exclusive access to ONE of these top AI stock picks, absolutely free!

More reading

- Prediction: these FTSE 100 and FTSE 250 trusts can beat the market in 5 years

- I asked DeepSeek for 3 top S&P 500 growth shares and its last pick made me laugh

- Why the easyJet share price could take off in 2025

- The Eurasia Mining (EUA) share price has jumped 43%. Time to buy this penny share?

- £20,000 invested in Amazon shares just 3 months ago would now be worth…