Is Palantir stock the new Nvidia? Why UK investors should (or shouldn’t) care

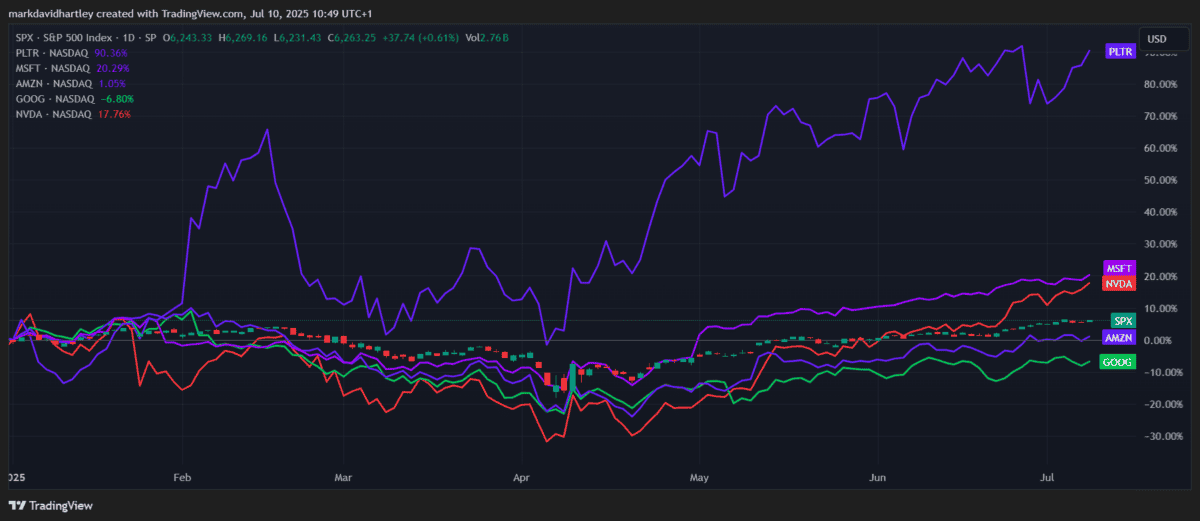

Palantir (NASDAQ: PLTR) stock’s enjoyed a spectacular run this year. The US data analytics and artificial intelligence (AI) specialist has seen its shares soar roughly 88% in 2025, making it the best performer on the S&P 500. By comparison, America’s darling chipmaker Nvidia’s up only 20%.

But while both companies are riding on the coattails of AI, they’re vastly different businesses. In the data analytics space, Palantir competes more closely with the likes of Microsoft, Amazon and Google.

Microsoft’s Azure and Amazon Web Services offer powerful data platforms with vast customer bases. Google’s AI expertise also poses a threat. These tech titans have deeper pockets and broader ecosystems, challenging Palantir’s long-term market share.

But as shown in the graph above, it’s leaving these rivals in the dust too.

So what’s fuelling the Palantir stock surge?

Government contracts are a big driver, with Palantir’s AI-driven solutions being used in sectors like healthcare, energy and automotive. In Q1 2025, these contracts helped contribute to an overall revenue jump of 39% to $883.9m.

Some analysts also point to the company’s clever branding and a cult-like following, attracting waves of retail investors in a meme-like manner.

More recently, it formed a strategic partnership with Accenture to streamline federal operations and is developing software for the US Navy dubbed ‘Warp Speed for Warships’.

Clearly, it’s a tech powerhouse with no plans to slow down.

But there are risks

High-growth tech stocks are inherently risky. First, Palantir’s valuation’s eye-watering, with a forward price-to-earnings (P/E) ratio north of 200, dwarfing Nvidia at only 37. That means growth expectations are sky-high and any misses could bring the house of cards tumbling down.

Second, more than 42% of its Q1 revenue came from US government contracts. Any change in defence budgets or shifting administrative priorities could hurt future profits.

Third, while the Accenture partnership and naval software are promising, it lacks the established credentials of mega-cap AI peers. Palantir only entered the Russell 1000 list recently and evidence of sustainable, long-term growth’s limited.

Should we consider it?

It depends on each investor’s individual risk appetite. There’s no denying the allure of a business at the heart of defence, AI and big data. If it can continue landing landmark contracts and broaden its commercial reach, today’s lofty valuation might not look so outlandish in hindsight.

It certainly ticks many high-growth boxes: big margins, strong government ties and notable potential in the exploding tech sector. But its hyper-valuation and reliance on politically sensitive contracts mean price swings could be extreme.

For investors looking to allocate a small portion of their portfolio to speculative high-risk growth, it’s worth considering — especially as a hedge alongside steady FTSE 100 income stocks.

But the more risk-averse — with a view for disciplined, long-term value — may prefer firms showing organic, multi-year revenue growth at more conservative valuations.

For me, great stocks combine strong underlying businesses with valuations that leave room for error. Right now, Palantir ticks the first box in spectacular fashion. The second? Not so much. As always, it pays to balance excitement with discipline.

The post Is Palantir stock the new Nvidia? Why UK investors should (or shouldn’t) care appeared first on The Motley Fool UK.

Passive income stocks: our picks

Do you like the idea of dividend income?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

If you’re excited by the thought of regular passive income payments, as well as the potential for significant growth on your initial investment…

Then we think you’ll want to see this report inside Motley Fool Share Advisor — ‘5 Essential Stocks For Passive Income Seekers’.

What’s more, today we’re giving away one of these stock picks, absolutely free!

More reading

- £10,000 invested in Palantir stock 5 years ago is now worth…

- £10,000 invested in Palantir stock 2 years ago is now worth…

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Mark Hartley has no position in any of the shares mentioned. The Motley Fool UK has recommended Alphabet, Amazon, Microsoft, and Nvidia. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.