Meet the FTSE 250 housebuilder I’m buying for my Stocks and Shares ISA in Q4

Vistry (LSE:VTY) is a name Iâve been focused on in my Stocks and Shares ISA recently. And Iâm expecting to keep buying until the end of the year.

After falling 48% in a year, the stock looks cheap. But I think there are some strong reasons for thinking the company could do very well in 2026.

UK housing

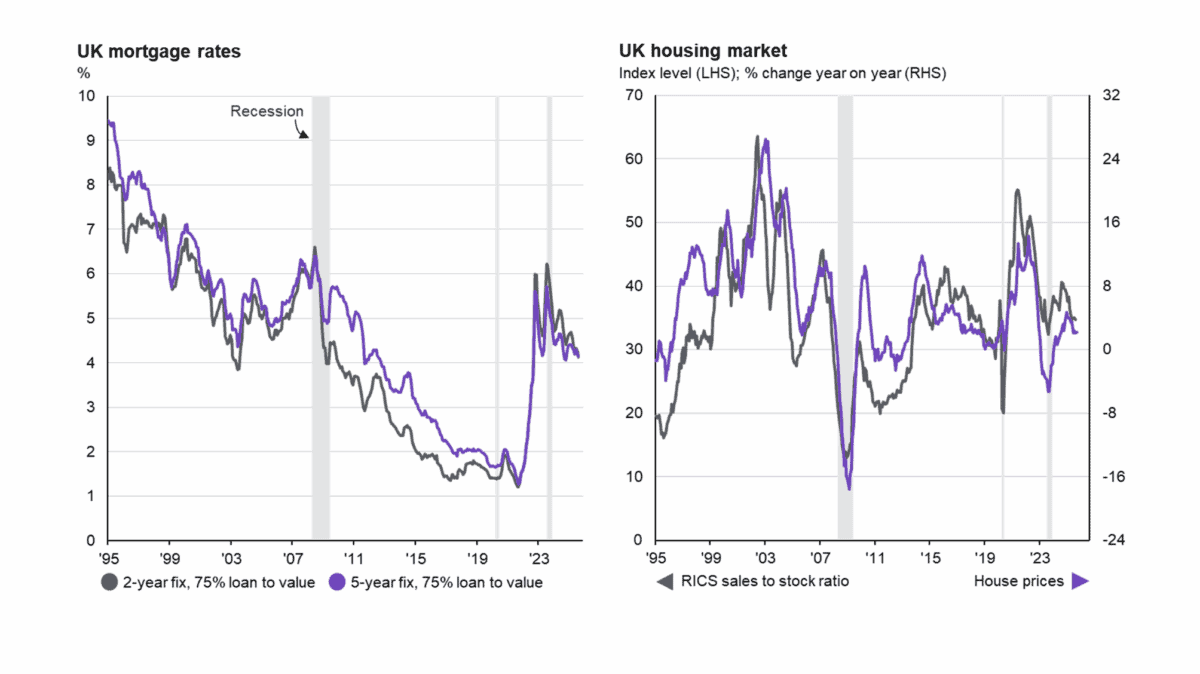

The UK property market is in a difficult position at the moment. Despite mortgage rates being at their lowest levels in three years, the ratio of sales to inventory levels has been falling recently.

Source: JP Morgan Guide to the Markets Q4 2025

Thereâs an obvious reason for this. The Budget is coming up in November and thereâs a lot of speculation about how the Chancellor is going to make ends meet.

The expectation is for tax increases of some sort, but thereâs still a lot of uncertainty. And this understandably makes people cautious about taking out big loans to buy houses.

By 2026, however, things should be much clearer. So Iâm hoping this will get the property market moving as it becomes easier for people to make buying decisions.

Profit warnings

An improving property market should help housebuilder stocks across the board next year. But there are also reasons for thinking Vistry is a particularly attractive candidate.

The firm has been dealing with some short-term issues that are entirely of its own making. Costing errors in one of its divisions meant a significant hit to profits in the companyâs 2024 financial year.

Those are set to continue, but the effect should be much lower in 2025 and 2026. The cost in 2025 should be around £30m â down from £91m â and then £5m in 2026.

Thatâs why Vistry is the housebuilder Iâm focusing on right now. I think the combination of margins expanding while revenues grow could be a powerful one for the business and the stock.

Risks

Rather than building houses to sell on the open market, Vistry focuses on partnering with housing associations and local authorities. I like this strategy, but it comes with its own risks.

The most obvious of these is it makes the company more reliant on public sector funding. While the government has been looking to support affordable housing projects, this canât be guaranteed.

Selling properties to partners who buy in bulk can also create challenges when it comes to pricing power. And thatâs a disadvantage of the guaranteed offtake that comes with Vistryâs model.

The positive, however, is that the firm has lower capital requirements than other builders. And I ultimately expect this to be an advantage when it comes to returning cash to shareholders.

Iâm a buyer

Unlike other UK builders, Vistry doesnât currently pay a dividend. In a stock market where shares in housebuilding companies come with high yields, this can mean it goes under the radar.

I think, however, that the stock is more attractive at the moment. In the near future, I expect lower costs and an improving property market to give the firm a big boost.

I also see the firmâs business model as a unique strength over the long term. Thatâs why Iâm looking to keep adding to my investment, held in my Stocks and Shares ISA, before the end of the year.

The post Meet the FTSE 250 housebuilder I’m buying for my Stocks and Shares ISA in Q4 appeared first on The Motley Fool UK.

Should you invest £1,000 in Vistry Group Plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Vistry Group Plc made the list?

More reading

- Here are 37 gold stocks I’ve ‘bought’ as bullion prices soar!

- Tesco shares reach new 18-year highs! Time to buy in?

- How much do you need in an ISA to aim for a £10k annual passive income?

- Why the HSBC share price spiked 10% last month

- By 2026, the Tesla share price could turn £5,000 intoâ¦

Stephen Wright has positions in Vistry Group Plc. The Motley Fool UK has recommended Vistry Group Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.