£1,000 buys 219 shares of this red-hot UK industrial stock that’s outperforming Rolls-Royce

Rolls-Royce shares continue to deliver fantastic returns for investors. Over the last year, theyâve risen about 65%.

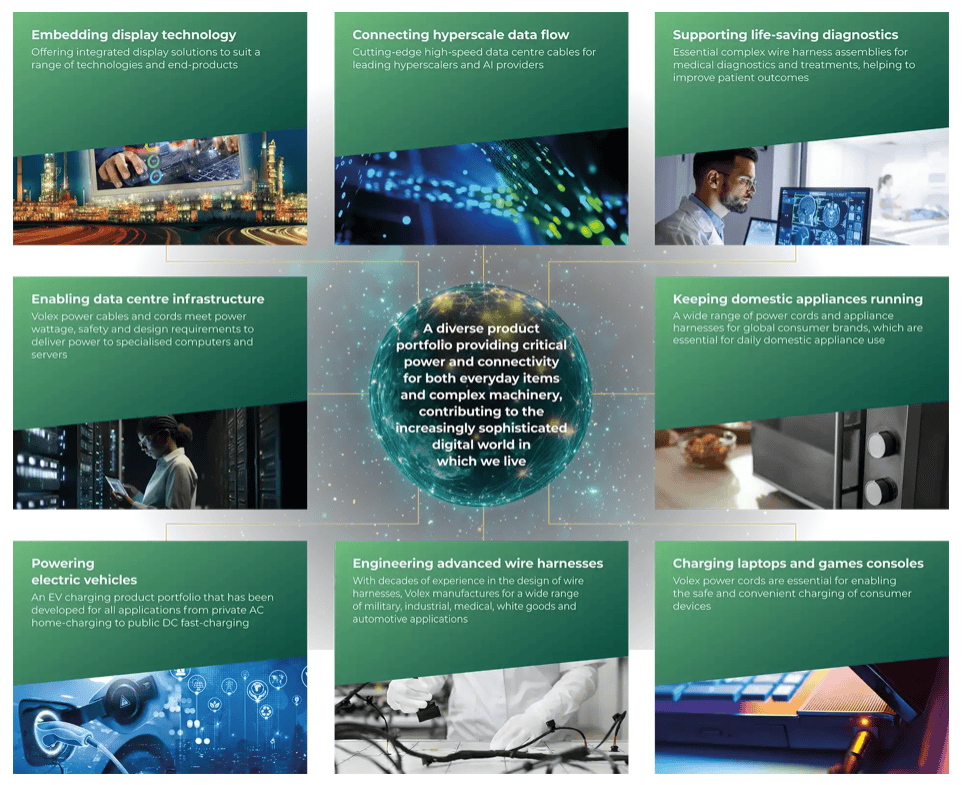

But investors could have generated higher returns with shares in a smaller British industrial company (that few people have heard of). This company specialises in manufacturing components for electric vehicles (EVs), medical equipment, and data centres and right now, itâs having a lot of success.

A UK company with momentum

The stock in focus today is Volex (LSE: VLX). Itâs a UK-based global manufacturer of power cords, cables, and data connectivity products for âmission criticalâ applications.

This company can trace its roots back to 1892 when two entrepreneurs started a manufacturing company in Manchester. It has come a long way since then â today it has 25 manufacturing sites across the world and over 13,000 employees.

At present, the companyâs share price is around £4.55. That means that £1,000 buys 219 shares (ignoring trading commissions).

In terms of performance, the shares are up about 35% (versus 18% for Rolls-Royce) over the last six months and about 67% over the last year. They still look pretty cheap though, especially compared to Rolls-Royce.

An investment opportunity?

In my view, this stock has a lot going for it right now. For a start, the company is growing at an impressive pace thanks to its strategy of focusing on manufacturing products for structural growth markets (eg, data centres and EVs).

In January, it advised that for the first nine months to December 2025, group revenue was $902.7m, representing year-on-year organic constant currency growth of 14.8%. It noted at the time that it was benefitting from particularly strong growth in its Complex Industrial Technology division, where it makes cables for data centres.

On the back of this performance, management said that full-year revenue (for the year ending 31 March) would be ahead of market expectations. It added that operating profit would be ahead of the Boardâs previous expectations.

We also have an attractive valuation. Looking at the earnings forecast for this financial year (38 cents), the price-to-earnings (P/E) ratio is just 16.

That seems very reasonable to me. Note that Rolls-Royce currently has a P/E ratio of about 40.

One other thing to highlight is the fact that in early February, Chief Operating Officer John Molloy bought 31,620 shares in the company at a price of £4.55 (todayâs share price). This trading activity suggests that the insider expects the share price to keep rising (no director buys company stock if they expect it to tank).

Worth a closer look

Iâll point out that this company is economically sensitive. If we were to see a major economic slowdown in the years ahead, Iâd expect its shares to underperform.

Its fortunes are also tied to certain industries. If, for example, the data centre industry was to experience a slowdown, growth could be compromised.

All things considered though, the risk/reward skew looks attractive to me. I believe this under-the-radar growth stock is worth a closer look right now.

The post £1,000 buys 219 shares of this red-hot UK industrial stock thatâs outperforming Rolls-Royce appeared first on The Motley Fool UK.

Should you invest £1,000 in Volex plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Volex plc made the list?

More reading

- A once-in-a-decade opportunity to buy BAE Systems shares ‘cheaply’?

- A once-in-a-decade chance to buy Nvidia stock on a P/E ratio of less than 20?

- How did the FTSE 100 near 11,000 so quickly?

- Here are 5 things Greggs shareholders just learned

- Lloyds’ share price has plunged 14% from its highs! Time to buy?

Edward Sheldon has no positions in any shares mentioned. The Motley Fool UK has recommended Rolls-Royce Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.